If you have a quick release from Fannie Mae and Freddie Mac, you may want to be patient.

While the chances that the pair coming out of the tutelage has increased sharply once Trump’s second term, he still faces a difficult battle.

One of the main bonding points is mortgage rates, which many expect to increase if they are released.

Having an almost explicit guarantee that Fannie and Freddie will buy and secure mortgages makes them cheaper for consumers.

The wait is that if / when they make it public, mortgage rates should be higher to compensate for the increased risk.

Fannie and Freddie have been in guardianship since 2008

First a quick background. After the worst housing crisis in recent history, Fannie Mae and Freddie Mac, known as Enterprises sponsored by the Government (GSES) placed in the guardianship.

It was essentially a bailout of the government because the pair was “seriously damaged” following the mortgage merger in the early 2000s and “unable to fulfill their missions without government intervention”.

The arrangement has enabled them to continue to support the very fragile housing market during its recovery in the last decade.

But perhaps no one expected the couple to stay in the hands of the government as long as they have done.

Lastly, it’s been almost 20 years now! Of course, this is not the first time that efforts have been made to put them back in nature.

During Trump’s first term which started in 2017, there were a lot of discussions on a release. And the actions of the two companies responded accordingly.

They were negotiated in the $ 1 range at the end of 2016 and quickly increased to more than $ 4 per share in early 2017 before discoloving again.

Once the privatization of Fannie Mae and Freddie Mac has lost steam, they finally became stocks of Penny.

Many investor speculation surround their release

As eight years ago, there was a lot of investor speculation surrounding their release, which is undoubtedly part of the problem.

It seems that people are more interesting to make money on a profession than to consider the real involvement of their release. Go understand …

The last speculator to participate in the apparent gold rush was the investor Bill AckmanIncluding the Pershing Square capital management company “could have around 180 million ordinary shares of the two companies”.

And he could have seen a billion dollars on the investment, the shares potentially amounts to around $ 34 post-compliance.

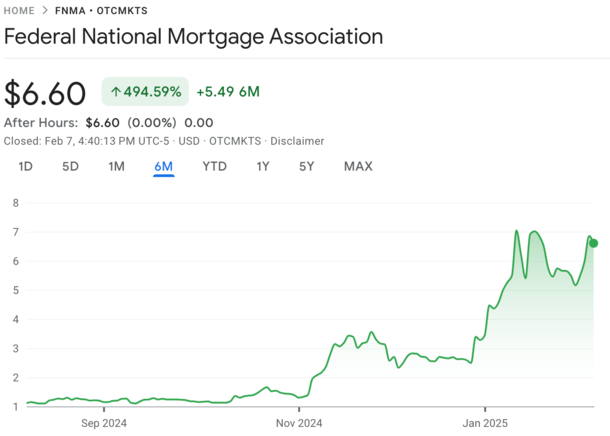

For reference, they are currently negotiating at around $ 6 each, so that would completely represent the gain.

Similar to the conditions before Trump’s first presidential victory, the couple negotiated in the $ 1 range.

But they have since soaked, with both Fnma And FMCC About 500% since Trump won a second term and speculation about their release reached euphoric levels.

As indicated, this is the conflict of interest currently at stake. And the same problem we saw eight years ago. It’s a scholarship instead of a “Hey, is it good for our country?”

Fannie and Freddie’s release will depend on the impact on mortgage rates

While investors hope that the pair will be released and make them incalculable wealth, We must only release them when it is safe and appropriate to do so.

If the secretary of the Treasury newly appointed Scott Bessent, who is, moreover, the new interim director of the Consumer Financial Protection Bureau (CFPB) also does the right thing, it may not be for a while.

In an interview with Bloomberg this week, when they asked them about their release, Bessent said“Right now, priority is tax policy. Once we have crossed this, we will think about it. »»

He added that “the priority for a release from Fannie and Freddie, the most important metric that I look at is any study or index that mortgage rates would increase.”

“So everything that is done around a safe and solid version will depend on the effect of long -term mortgage rates.”

In simple terms, he and those around him know that mortgage rates will probably increase if Fannie and Freddie are forced to stand alone.

And because mortgage rates went from around 3% to start 2022 to around 7% today, the last thing that the Trump administration wants is higher rates.

So, really, it comes down to helping investors become rich or helping Americans on a daily basis buy houses with lower mortgage rates.

Will be an interesting decision …

The pair must be released, but perhaps slowly after having reduced their imprint

My thoughts on the question are that the pair is not ready to be released. Little has changed since they went under the supervision, apart from the quality of the mortgage, improvement considerably.

Of course, they do not have as much concerns concerning the defects of mortgage loans and seizures, but they also continue to support the vast majority of real estate loans in the United States.

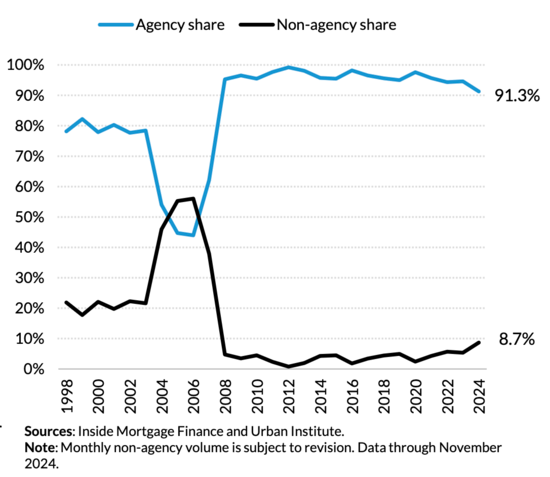

Look at a graphic above Urban institute. More than 91% of the MBA issue is supported by the agency, which also includes the FHA and VA. But around 40% of the origins of the first-lien are GSE, while 4.1% are private.

Without them, there would be chaos on the mortgage market. Even if he was released, there would probably be chaos.

However, they should be released at some point if they are truly public companies and not government entities.

A better way to proceed can be considerably reduced their footprint before it happens (sorry investors).

To do this, they can go completely back or stop buying and securing mortgages related to secondary residences and investment properties.

In other words, limit their options to primary residences for daily owners as opposed to those who buy a second, third, fourth or even fifth home.

Ironically, this could also release the offer for sale, which has tormented the housing market for at least the last decade.

There could be additional changes to their product menu, which would make it smaller, with the implicit aim of infiltrating more private capital on the mortgage market.

As Fannie and Freddie become smaller, private players could grow and play a role more.

This would reduce our dependence on the pair and reduce the impact of their possible version.

(photo: Virginia state parks))

Before creating this site, I worked as account manager for a wholesale mortgage lender in Los Angeles. My practical experience in the early 2000s inspired me to start writing on the mortgages 19 years ago to help potential (and existing) buyers better navigate in the mortgage process. Follow me on X for hot catches.