Although 2025 gives hope for a drop in mortgage rates, this is still very uncertain.

There are renewed fears that inflation could pick up, pushing rates higher in the new year.

Especially as we welcome a new president who has promised to introduce inflationary policies, such as across-the-board tariffs.

This affects not only potential homebuyers struggling with affordability, but also existing homeowners looking to refinance.

After all, millions of people still managed to get mortgages when rates were between 7 and 8 percent, and they are rightly looking for relief.

How can we make the decision to refinance a little easier?

One thing I want to point out first is that there is no general rule of refinancing. Of course, I wish there was.

It would be great if you could make a general statement to help owners decide whether they can benefit from this or not. But that’s simply not the case.

There are far too many variables involved in mortgages and real estate to do this. But we can at least give you some advice to make the decision easier.

Today, I focus on rate and term refinances, which allow borrowers to exchange their old loan for a new one with a lower interest rate and new term.

It’s pretty much the only game in town right now, as cash-out refinances don’t make much sense given that the rates aren’t that attractive.

Either way, one thing to consider when making a refinancing decision is the amount of your outstanding loan balance.

Simply put, a larger loan amount makes refinancing much easier because it results in greater savings.

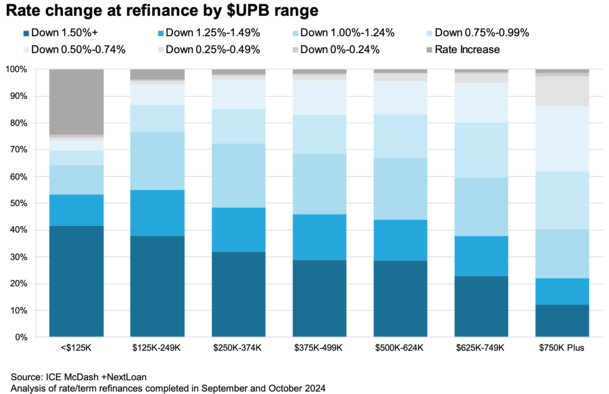

Homeowners with larger loans need fewer rate movements to refinance

Most recent ICE Monthly Mortgage Monitor does an excellent job of illustrating how loan amounts affect refinancing decisions.

They noted that for most borrowers with loan balances below $250,000, a rate reduction of at least 125 basis points (1.25%) was needed to move forward and submit a request.

In other words, if their rate were 7.75%, it would have to be at least 6.5% to make refinancing worth it. Obviously, this can be a pretty big question because it’s a significant spread between rates.

Fortunately, mortgage rates fell to these levels in August and September, before rebounding after the Fed lowered its own rate.

Regardless, on the other end of the spectrum were people with loans of at least $750,000.

For this cohort, they could act on a mortgage refinance with much less incentive. ICE found that about 40% of them lowered their rates by only 75 basis points or less.

From say 7.25% to 6.5%. And an additional 12% of these larger borrowers thought refinancing was worth it at a rate less than 50 basis points lower.

In other words, going from 7% to 6.5%. That doesn’t seem like much, does it?

Finally, for those with a very small loan amount, thinking less than $125,000, we actually support increasing their mortgage rate, with about 25% of them opting for this option.

For what? Well, they probably went for a cash-out refinance because they needed the money. And because their loan amount was small, they had less incentive to keep the old loan.

This works against those who have larger loans at 2-4% and face a mortgage rate lock-in.

Let’s do the math to find out why loan amounts matter for your refinancing

| Loan amount of $250,000 | Loan amount of $750,000 | |

| Old mortgage rate | 7.75% | 7.25% |

| Old payment | $1,791.03 | $5,116.32 |

| New mortgage rate | 6.50% | 6.50% |

| New payment | $1,580.17 | $4,740.51 |

| Difference | $211 | $376 |

Taking the two loan scenarios I presented above, we have a borrower with a loan amount of $250,000 and a mortgage rate of 7.75%.

They see that it is possible to refinance up to 6.50%, which represents considerable progress in terms of rates. But how much does this really save them per month?

Only about $211 per month. This is not an incidental amount, but it illustrates why a significant rate change was necessary to make the associated or upfront costs worthwhile.

Remember, you want to hold the loan long enough to justify the closing costs involved in the transaction.

Next we have our $750,000 borrower with a rate of 7.25% who is refinanced to 6.50%.

This results in almost double savings ($376) compared to the other borrower, despite a much smaller rate improvement.

The caveat here is that the borrower with the lowest loan amount might consider $200 to be as valuable a savings, if not more, than the borrower with the highest loan amount who has saved almost $400 $.

But if someone tries to tell you that rates need to drop by X amount to make your refinancing worth it, ignore them.

Instead, take the time to do the math to see exactly how much you can save. Or maybe don’t save!

There’s no shortcut if you want to save money on your mortgage. However, if you put in the time, the return on investment can be pretty incredible.

(photo: The Harry Manback)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to start writing about mortgages 18 years ago to help potential (and existing) buyers better navigate the home loan process. Follow me on Twitter for hot takes.