Personal loans can be the most helpful financial solution for anyone who needs extra funds for a large purchase, family event, or unforeseen emergency.

But let’s say you’re planning a wedding and find a great loan offer, only to find out later that your interest is higher than expected. So how can you make sure you’re not paying more than you need to?

The above scenario is all too common and interest rates significantly influence the cost of the loan. This shows us how important it is to understand personal loan interest rates before deciding to take out a loan.

Read on to know more about personal loan interest rates in India.

The interest rate on a personal loan corresponds to the cost of borrowing and is generally expressed as an annual percentage. When you take out a loan, you are charged interest on the amount borrowed, and when you save or invest money, you earn interest. Interest rates are influenced by factors such as central bank policies, demand for credit and economic conditions. These fluctuations have a significant impact on consumer spending, investment choices and economic activity in general.

The personal loan interest rate is one of the most important factors that determine the total cost of borrowing. This directly affects the monthly payments and overall affordability of the loan. We have provided the personal loan interest rates and other fees charged by LoanTap here:

| Costs | Applicable fees |

| Interest rate | Up to 26% |

| Processing Fees | 2%-3% + GST |

| Bounce Fees | ₹550 |

| Prepayment Fee | 4% + GST if seized within 180 days from the date of disbursement after the cooling-off period |

| Platform Fees | ₹750 + GST |

| Interrupted Period Interest / Pre-EMI Interest | Depends on disbursement date |

How to calculate the interest on a personal loan?

Calculating the amount of interest payable on a personal loan is essential to understanding the total cost of borrowing and planning your finances effectively.

The easiest way to calculate the interest amount on personal loans is to use an online EMI calculator.

Here you just need to add your chosen loan amount, interest rate and repayment term. The EMI calculator will automatically calculate your monthly loan EMI and total interest payable.

The other way is to manually calculate the interest amount for personal loans. To do this, you can use the following formula:

Total interest = Total amount – Principal

Let’s use this formula in an example to understand it better.

Suppose Mr. Raj takes a personal loan of Rs. 4 Lakh at an interest rate of 14% per annum to be repaid in 2 years.

To solve this problem, let’s break down the information provided:

Loan Amount (Principal, P) = Rs. 4,00,000

Annual interest rate (r) = 14% or 0.14

Loan duration (n): 2 years or 24 months

To calculate the monthly EMI, we will first convert the annual interest rate into monthly rate and the tenure into months:

Monthly interest rate (r) = Annual rate / 12

0.14/12 ≈0.01167

Duration of occupancy in months (N) = 2 years × 12 = 24 months

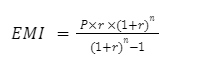

- EMI Calculation

Using the EMI formula:

2. Total amount to pay

The total amount to pay is simply:

Total amount = EMI X n

3. Total interest payable

The total interest payable can be calculated by subtracting the principal from the total amount:

Total interest = Total amount – P

Now let’s calculate these values.

Here are the values calculated for Mr. Raj’s loan:

- Monthly EMI: Rs. 19,205.15

- Total interest payable: Rs. 60,923.68

- Total amount payable: Rs. 4,60,923.68

Factors Affecting Personal Loan Interest Rates

When applying for a personal loan, understanding the factors that influence your interest rate can help you get better terms. Here are some factors lenders consider when determining your loan interest rate:

Monthly income

Your monthly income is one of the most important factors that affect both the amount you can borrow and the interest rate you receive. Higher income reduces the lender’s risk because it indicates your ability to repay the loan consistently. Lenders are more likely to offer lower interest rates to borrowers with stable, substantial incomes because they consider these individuals to be less likely to default on their repayments.

Credit score

Your credit score reflects your creditworthiness and financial responsibility. A high credit score indicates that you manage your finances well, which makes you a more attractive borrower. Generally, borrowers with a credit score above 700 may qualify for lower interest rates, while those with lower scores may face higher rates due to perceived risk.

Loan repayment history

Your previous loan repayment history is examined, as well as your overall credit score. Lenders check to see if you have a history of making timely payments. A consistent history of on-time EMI payments suggests that you are a responsible borrower, which can result in more favorable interest rates for your personal loan.

Additionally, a history of defaults can impact your ability to get a personal loan. If you have a history of defaulting on payments, the lender may either deny your application or charge significantly higher interest rates to mitigate the risk associated with the loan granted to you.

Debt-to-income ratio

The debt-to-income ratio (DTI) is an important statistic that tells the lender how much of a borrower’s income is going toward monthly debt payments. A DTI of 30% or less is considered favorable by lenders and may result in lower interest rates on personal loans.

Tips for availing personal loans at low interest rates

Getting a personal loan at a low interest rate involves a combination of good financial habits and strategic planning. Here are some tips for getting personal loans at low interest rates:

1. Maintain a strong credit score

A good credit score is important for obtaining a personal loan. You must maintain a credit score of 700 and above to increase your chances of obtaining a personal loan on favorable terms. To maintain a good score:

- Pay your bills on time: You must ensure that all your dues and debts, including credit card payments, are paid on time each month.

- Manage credit usage: Keep your credit utilization rate below 30%. This indicates that you are not overly dependent on credit.

- Limit new credit applications: Avoid applying for multiple credit cards or loans in a short period of time, as this can negatively impact your score.

- Monitor co-signed loans: Be sure to pay any co-signed loan in a timely manner, as defaults can affect both your credit score and that of the primary borrower.

- Pay off credit cards in full: Avoid interest charges by paying your credit card balance in full each month, demonstrating responsible credit habits.

2. Shop for the best rates

Don’t settle for the first lender you find. You need to do thorough research to find competitive interest rates:

- Compare offers: Compare loan amounts, fees and more from different lenders.

- Negotiate with existing lenders: If you have a positive history with your current bank or NBFC, ask about their personal loan offerings as they may offer lower rates to loyal customers.

3. Evaluate your work history

Your job stability also helps determine your personal loan interest rate. Here’s what you need to consider:

- Job stability: Lenders prefer candidates with at least two years of work experience, including one year with the current employer.

- Fixed bond/income ratio (FOIR): A lower FOIR indicates that your monthly obligations are manageable relative to your income, making you a less risky borrower.

- Type of employment: Being employed in a reputed organization, especially in the government or PSUs, can enhance your application. Lenders view these positions as more stable, which may result in lower interest rates.

Conclusion

Understanding personal loan interest rates in India is essential for making informed financial decisions. By being aware of the factors that influence these rates and exploring options from different lenders, you can get an interest rate on your personal loan that best suits your financial situation. Whether you’re borrowing for personal goals or for emergency expenses, knowing the total cost of a loan can help you avoid unnecessary financial stress.

If you are looking for a competitive personal loanLoanTap offers a range of loan products with attractive interest rates and minimal documentation requirements. With fast processing times and flexible repayment options, LoanTap makes borrowing simple and affordable, ensuring you have access to funds when you need them most.

Frequently Asked Questions

What factors influence personal loan interest rates in India?

A person’s credit score, income, repayment history, and lender’s policies are some of the variables that affect personal loan interest rates.

How can I improve my chances of getting a lower interest rate?

You can increase your chances of getting lower interest rates on your personal loan by maintaining a high credit score, comparing rates from multiple lenders, and demonstrating a stable source of income.

Is the interest rate on personal loans fixed or variable?

Depending on the type of loan and the terms offered by the lender, personal loan interest rates in India can be fixed or variable.

Do early or early repayments affect the interest rate?

No, early or early repayments do not directly affect the interest rate; however, they can reduce the total interest paid over the life of the loan.

How does my credit score impact the interest rate I receive?

Since a higher credit score indicates less credit risk for the lender, interest rates on personal loans are often lower.

Related blogs

Fixed interest rate or reduced interest rate: which is better?

08/11/2024

![]()

List of Fake Loan Apps in India 2024 – How to Identify and Avoid Scams

07/11/2024

![]()

TDS on interest on unsecured loan

10/23/2024

![]()