It is not a secret inventory for sale has been in need for a long time now, which makes it increasingly difficult to find the house of your dreams.

The offer of available houses has dropped considerably when the pandemic has settled, but since the beginning of the beginning of 2022, it has increased to a fairly stable clip.

The obvious engine of the increase in supply for sale was much higher mortgage rates, which led to more houses on the market.

This is mainly attributable to a lack of affordability, which has become worse than the conditions observed in the early 2000s.

But there is still a great variance in the supply levels throughout the country, the South and the Southeast given an overabundance while supply in the Midwest and the North East remains rare.

The available offer is at the origin of the housing market

Although many people think that mortgage rates stimulate the prices of houses, which is higher, is not really true.

Of course, there are indirect higher interest rate effects, such as reduction in purchasing power, which in turn can lead to fewer buyers.

And fewer buyers means less demand, which can increase the supply if more houses are seated on the market.

But if you consider that the whole country has essentially access to the same mortgage rates, it is clear that rates are only a contributory factor.

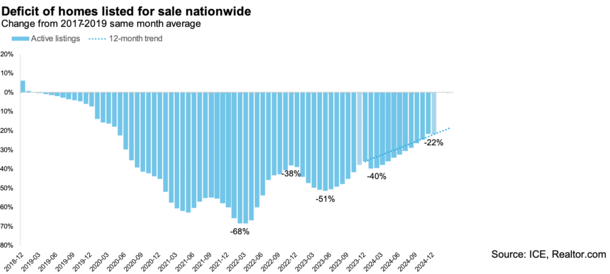

The last Ice mortgage monitor report revealed that the number of active registrations increased by 22% by 22% last year.

This pushed the national lists deficit of -36% at -22%, which means that there are still too few houses for sale, but it is not as bad as it was.

In addition, we are now in progress to return to the pre-countryic levels of inventory for sale by mid-2026.

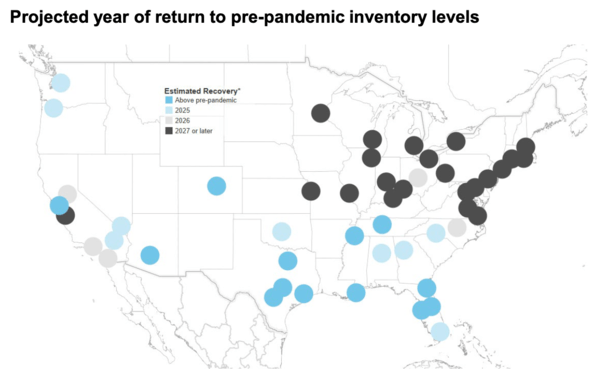

Of course, it is on a national basis, and looking at things at the national level is not so useful for people who envisage a house purchase in a specific metro.

Housing supply is mainly back to normal in southern and southeast

Take south and south-east, which includes tastes of Florida and Texas, long on the radar of the housing bear to be at risk of a correction of the price of houses.

About 25% of the main national markets are already back at pre-Pandemic supply levels, and most of them are located in southern and southeast.

15% of the additional markets are being “standardized” this year, which means that almost half of the United States will have an adequate supply. And at the moment, it is especially in the southern half of the country.

When we have taken into account the worst affordability for decades, mainly equally with the peak of housing bubbles in 2006, this could be a problem.

As indicated, the conditions are already quite unaffordable, and if more of the offer is online, there will probably be downward pressure on the prices of houses.

On the one hand, it could be a good thing for potential buyers in these regions.

If the offer increases and the sellers drop their prices, the affordability will improve for those who seek to buy a house.

But on the other, this means that those who seek to sell will not be able to seek a high price, and it could be a problem for recent buyers.

So much so that we could see a return of underwater mortgages and low evaluations, which has been rare for a large part of the last decade.

But the supply remains tight in the Midwest and the Northeast

While the supply develops in states like Florida and Texas, it remains tight in the Midwest and the Northeast.

These regions continue to see limited stocks, which has led to high price gains.

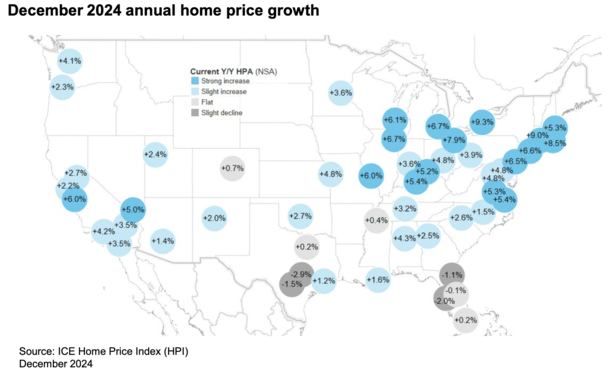

For example, the National Association of Realtors recently pointed out that the median prize in the Northeast had ended the year at $ 478,900, up 11.8% compared to last year.

The same goes in the Midwest, where prices increased by 9% in annual sliding.

Prices have also increased in the South and West, but only 3.4% and 6%, respectively.

In other words, he continues to be a story of supply, with Nar note that there were only 3.3 months of nationwide supply to the current monthly sale rate.

It is below your 4 to 5 typical months for a healthy and balanced market.

But as we can see, it does not spread evenly throughout the country, so the conditions of purchase and sale will vary considerably.

A very branched housing market exists today

What is perhaps unique on today’s housing market, despite the sharing of the same unaffordable conditions observed in the early 2000s, this is the variance between the markets.

We have all heard the old line, “real estate is local”. And it couldn’t be more true today.

Certain markets in Florida and Texas already have active registration accounts higher than their pre-countryic levels.

Consequently, the prices of houses have dropped on an annual basis. Large metros like Austin, TX and Tampa, FL have seen the property values become already negative.

The prices of houses fell 2.9% in 2024 in Austin, followed from -2.0% to Tampa, -1.5% in San Antonio, -1.1% in Jacksonville and -0.1% in Orlando , by ice.

At the same time, prices jumped 9.3% in Buffalo, followed by 9% in Hartford, 8.5% in Providence and 7.9% in Cleveland and Detroit.

In short, it is very difficult to characterize the national housing market today as healthy or unhealthy, or as expensive or cheap.

It varies considerably depending on the market, so if you are a buyer of houses today (or a seller), it is imperative to know your local market and pay less attention to national figures.

Be that as it may, it seems that the inventory is on the path of normalization in most of the country.

Simply note that even the pre-countryic supply levels were not necessarily high, so even then the choice could remain limited.

And above all, without efficiency to the subscription of quick and loose mortgages, any price softening that we see today pale in relation to what we have seen then.

Read more: Sales of existing houses have come to the lowest levels since 1995

Before creating this site, I worked as account manager for a wholesale mortgage lender in Los Angeles. My practical experience in the early 2000s inspired me to start writing on the mortgages 19 years ago to help potential (and existing) buyers better navigate in the mortgage process. Follow me on X for hot catches.