This was good weeks for mortgage rates, which benefited from a delay on prices and some favorable economic data.

Between a slowdown in the economy, reduced inflation and the thought that prices could be exaggerated, bond return at 10 years has improved considerably.

Since reached its 2025 summit by 4.81% on January 13, it has since decreased 35 base points in less than a month.

This was motivated by cooler inflation / economic data and less for fear of prices and a broader trade war.

However, mortgage rates have not dropped from the same amount, which tells you that there is still a lot of defense on prices.

Mortgage lenders remain defensive on prices

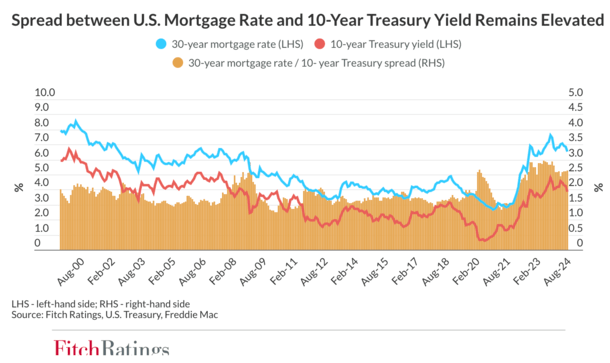

Bond return at 10 years is a good way to follow mortgage rates, with the fixed move of 30 years in locking relative over time.

However, over the past two years, mortgage rate differences (demand from MBS Premium investors) have increased considerably.

On a large part of this century, since at least 2000, the spread has oscillated around 170 base points on average.

At the end of 2023, it expanded to around 300 basic points (BPS), which means that investors demanded a full difference of 3% above comparable treasure bills, as shown in the graph -dessus from Fitch dimensions.

This was largely motivated by the risk of early repayment and, to a certain extent, credit risk, such as loan failure.

But I suppose that it is mainly preparations that MBS investors fear, because mortgage rates have almost tripled in about a year.

In other words, thought was that these mortgages would not have much shelf life and would be refined as soon as possible.

Propagation has since arrived a little, but is still around 260 bps, which means that it is nearly 100 bps above its long-term average.

In simple terms, the price remains very cautious compared to the standard, and this has worsened in the past two weeks.

The Spreads actually approached the level of 200 BPS before climbing recently again.

Is there too much volatility for a flight to security?

As for why, I suppose that increased uncertainty and volatility. After all, Canada and Mexico had to face prices last week before being “delayed”. But prices on China are still in force.

While the market has generally applauded this development, which can say that it does not change in a week?

The same goes for all government agencies to be suspended or closed, or the buyouts given to federal employees.

For the lack of a better word, there are a lot of chaos at the moment, which does not increase well for mortgage rates.

They say that there is a flight to security when the stock market and a broader economy are unstable or volatile, where investors abandon the shares and buy obligations.

This increases the price of bonds and reduces their return, AKE interest rate. This is also good for mortgage rates according to the same principle.

But there is a certain point where the conditions are so volatile that the obligations and the actions become defensive at the same time.

Both can sell and no one really benefits, consumers seeing the wealth effect fading while faced with higher interest rates.

(Mortgage rate against the stock market)

The 30 -year -old fixed could be at the bottom 6s today

The big question is when can we see a certain stability on the bond market and MBS, which would allow the spreats to finally penetrate?

Some say that the yield at 10 years at around 4.50% today is quite reasonable given the current economic conditions.

If this goes to more or less stay, the only other way to obtain lower mortgage rates is compression of propagation.

We know that the gaps are swollen and have room to descend, so it is what will be necessary except for a contracting economy or less well -to -down driving unemployment.

Assuming that the Spreads were even close to their recent standards, let’s say 200 basic points greater than 10 years, we already had a fixed of 6.5% of 30 years. Maybe even a rate of 6.375%.

Those who have chosen to pay discount points could probably obtain a rate that started with a “5” and which would not be half bad for most new house buyers.

It would also be attractive enough for those who bought a house from the end of 2022 to 2024, which could have an interest rate of 7 or 8%.

In other words, there are a ton of opportunities just darkest. Much of the heaviness on the fight against inflation has already been carried out.

So if we can get there, a relief from the borrower is on the way. And mortgage lenders who have traveled water and barely survive in recent years will eventually be saved.

We just need messaging and a clearer policy of the new administration, which will allow investors to leave their too defensive position.

Before creating this site, I worked as account manager for a wholesale mortgage lender in Los Angeles. My practical experience in the early 2000s inspired me to start writing on the mortgages 19 years ago to help potential (and existing) buyers better navigate in the mortgage process. Follow me on X for hot catches.