As I said before when talking about mortgage, what a difference a week can make. Or even a few days.

If you’re new to mortgage rates, be aware that they can be very volatile. And can change from one day to the next.

Similar to a stock, the price might not be the same tomorrow (it might be higher or lower, or even unchanged).

On top of that, the price can even change several times a day, usually when there is a lot going on.

This happened today, with a price revision in the afternoon after rates had already improved compared to the day before.

Why did mortgage rates drop today (and yesterday)?

In short, weak economic data was the driver and falling mortgage rates were the beneficiary.

We received several colder than expected economic reports this week, including PPI, CPI, Initial Jobless Claims and Retail Sales.

It was essentially the best economic data anyone could hope for. And as we all know, weaker economic data leads to lower mortgage rates (and vice versa).

So if you’re in favor of lower mortgage rates, you unfortunately also have to somehow encourage a slowdown in the economy.

Granted, you don’t have to root for it to collapse, so it’s not entirely cynical to hope for some weakness.

Inflation has been high for years, and there’s nothing wrong with it falling while the economy continues to move at a more reasonable pace.

There is a happy medium, generally known as a “soft landing,” when the economy slows but does not slide into recession.

It remains to be seen what happens there, but if you’re curious about what mortgage rates do during a recession, I’ve written about that as well.

In addition to this data victory, the confirmation of new Treasury Secretary Scott Bessent took place today.

Bonds also rallied when it was first announced in November, and the market seems to like it again today.

He essentially saw the voice of reason in what could be a tumultuous administration. Additionally, he downplayed tariffs, calling them inflationary factors.

Finally, Federal Reserve Governor Christopher Waller rang say the Fed could cut rates faster and sooner if the inflation outlook remains favorable.

In short, these events have mitigated many of the reasons why mortgage rates have surged in recent months.

How much have mortgage rates improved?

Although it is difficult to get a perfect valuation, since not all banks and lenders offer the same rates, nor adjust them accordingly, we can at least evaluate it.

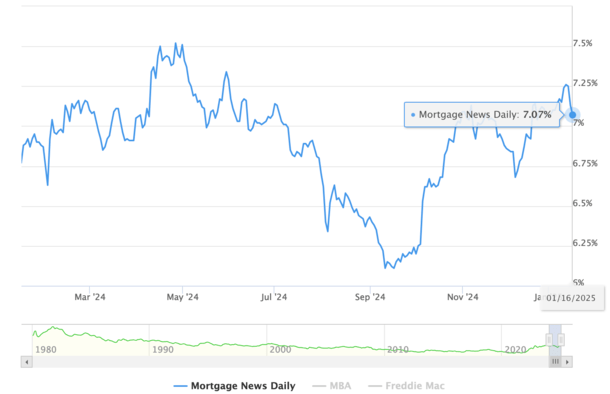

A great place to see daily rate trends in composite form is via Daily Mortgage Newswhich publishes 30-year fixed mortgage rates daily.

They showed a rate of 7.26% on Tuesday, the highest rate since May 2024!

Rates have since fallen to 7.07% as of today. And there is also a repricing in the afternoon as noted.

The first publication set the 30-year fixed rate at 7.11%, before an additional press release lowered it another four basis points to 7.07%.

In fact, most borrowers who lock in their rates now get loans starting with 6 instead of 7.

This is because real-time lock data from Optimal blue put the 30-year fixed rate at 6.96% as of Wednesday.

It probably also fell a decent amount today, which we’ll find out tomorrow. In other words, borrowers could lock in rates around 6.875% instead of 7.125% or 7.25%.

So maybe a weekly improvement from 0.25% to 0.375%, plus the psychological victory of going from 7 to 6.

Can the rise in mortgage rates continue?

The million dollar question is whether this can continue or whether it will experience an inevitable setback. It may not be inevitable.

If the data continues to cooperate and the new administration, which takes the reins on Monday, does not disrupt the markets, the recovery can continue.

And mortgage rates may continue to fall. It’s another question how far below we’ll be, but if data, like unemployment and inflation, turns out to be favorable, we could get back to where we were in September.

If you recall, the 30-year fixed rate was almost 6% at the time, just before the Fed ironically cut its own federal funds rate. Then we were hit with a hot jobs report, which made the pain even worse.

Assuming these things improve and inflation comes down and the job market doesn’t look as hot, mortgage rates could return to these levels.

But we also have to worry about government spending and Treasury emissions, which worry many people under Trump. Not to mention many other inflation-inducing ideas that may or may not come to fruition.

If you’re curious, I wrote about what could happen to mortgage rates during Trump’s second term.

The crucial point is that it depends on what he actually does versus what he said he would do, and how those actions will affect the economy.

But some of this responsibility could be beyond its control anyway, if, for example, we are already heading into a recession.

To summarize, like every other year, there will be opportunities as rates fluctuate, so if you are buying a home, pay close attention to rates each day.

Continue reading: Mortgage rate forecasts for 2025

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to start writing about mortgages 18 years ago to help potential (and existing) buyers better navigate the home loan process. Follow me on Twitter for hot takes.