The Consumer Financial Protection Bureau (CFPB) has finalized a rule that will remove medical debt from consumer credit reports.

In doing so, Americans’ credit scores are expected to increase by an average of about 20 points, increasing the number of home loan applicants who get approved for a home loan.

The agency noted that “medical debts provide little predictive value to lenders regarding borrowers’ ability to repay other debts.”

And are often flagged by consumers as inaccurate or controversial, resulting in more harm than good.

In the future, the inclusion of medical bills on credit reports will be prohibited and lenders will be prohibited from using medical information in their credit decisions.

No More Medical Debt Linked to Credit Reports

Specifically, CFPB’s new change will amend Regulation V removing an exception that allowed creditors to obtain and count medical debt in determining credit eligibility.

Thus, the Fair Credit Reporting Act (FCRA) will now prohibit creditors from considering medical information when underwriting new loans.

And credit reporting bureaus (Equifax, Experian, TransUnion) will not be able to provide lenders with consumer credit reports containing medical debt information.

Previously, the trio announced the removal of medical collections if the amounts were less than $500.

And the two major credit reporting companies, FICO and VantageScore, had adjusted their algorithms to reduce the impact of medical bills on a consumer’s credit score.

But now, all medical bills will be banned from credit reports, except for medical forbearance plans and medical expenses accompanied by a loan.

Lenders will also be prohibited from considering medical information, for example by requiring medical devices to be used as collateral for a loan in the event of repossession.

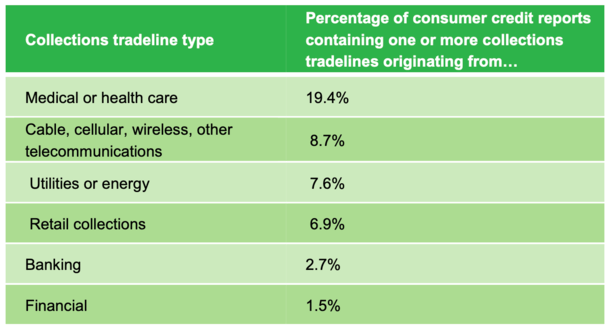

The CFPB found that commercial collection lines were present on nearly a third (31.6%) of credit reports, with medical debt accounting for about half (52%) of those.

As a result, nearly one in five consumers (19.5%) has one or more collection accounts from a medical provider on their credit report.

Long story short, you shouldn’t see much, if any, medical information on your credit report going forward.

But aren’t recoveries and medical charges already being ignored?

Prior to this new rule change, Fannie Mae, Freddie Mac, the FHA and VA had already updated underwriting guidelines for ignore medical collections and charge-offs.

This meant that even if they appeared on a credit report, they would not be factored into the borrower’s DTI ratio nor would they have to be repaid until the loan was funded.

While this provided some much-needed relief, the presence of medical debt on credit reports still meant that a borrower’s credit score may have been negatively affected.

As such, a hypothetical borrower could have seen their FICO score drop by 20 points or more, pushing them into a higher price range.

For example, a borrower with a FICO score of 695 is subject to a 1.75% price reduction for credit score alone.

Meanwhile, a borrower with a FICO 700-719 is only subject to a 1.375% price reduction.

This difference in loan cost is then passed on to the borrower in the form of higher closing costs or a higher mortgage rate.

For some potential borrowers, the lower credit score may have been enough to disqualify them from loan approval altogether.

22,000 additional mortgage approvals expected each year

With this new rule, the CFPB projects that 22,000 more Americans will be granted “affordable mortgages” each year.

This means that having a questionable medical bill will no longer be a barrier to homeownership.

This is largely because borrowers with medical debt on their credit reports see their average credit score increase by 20 points once that information is removed.

For example, if a borrower had a mid-range score of 680 before this change, they could have a FICO of over 700 in the future.

Keep in mind that until now, FICO and VantageScore still gave weight to medical debt in their scoring models, despite reducing the impact of such events.

They will now be prohibited from doing so, which, all things being equal, will result in higher credit scores across the board.

Additionally, borrowers may have had to provide a letter of explanation for medical collection in the past, which required more legwork and potentially jeopardized their approval.

This will no longer be the case, which should result in more loans being approved at lower mortgage rates, reflecting higher credit scores.

The CFPB also expects the removal of this special “carve-out” that allowed creditors to consider medical debts in order to increase privacy protections and reduce coercive debt collection practices.

So, aside from the fact that it may become easier to qualify for a mortgage, consumers will be less likely to be burdened by pesky debt collectors.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to start writing about mortgages 18 years ago to help potential (and existing) buyers better navigate the home loan process. Follow me on Twitter for hot takes.