I sometimes wonder, with so little equity extracted this cycle, if the real estate market is still in its infancy. At least as far as the next collapse is concerned.

Of course, housing sales volume has fallen due to unaffordable conditions, driven by high house prices and significantly higher mortgage rates.

But do we still need a flood of HELOCs and refi withdrawals before the market inevitably overheats again?

Otherwise, it’s simply an unaffordable market that will likely become more affordable as mortgage rates fall, housing prices stagnate, and wages rise.

Where’s the fun in that?

Owners were maxed out in the early 2000s

If you look at outstanding mortgage debt today, it actually hasn’t increased much over the last 16 years when the housing bubble burst.

It skyrocketed in the early 2000s, thanks to rapidly rising house prices and no-money-down financing.

And a flood of cash-out refinancings that went up to 100% LTV and beyond (125% financing, anyone?).

Basically, homeowners and homebuyers at the time borrowed every penny they could, and then some.

Either they cashed in on higher valuations every six months, fueled by low-quality real estate appraisals, or they took out a HELOC or home equity loan behind their first mortgage.

Many also purchase investment properties without a down payment, and even without any documents.

Regardless, home buyers at the time were still maximizing their borrowing capacity.

That was a bit of the approach at the time. Your loan officer or mortgage broker will tell you how much you can afford and you will maximize that amount. There was no reason to hold back.

If it wasn’t affordable, the reported income would simply be higher to make a pencil.

This phenomenon was compounded by faulty home appraisals, which allowed property values to rise higher and higher.

Of course, it didn’t take long for the bubble to burst and we saw an unprecedented flood of short sales and foreclosures.

Many of these mortgages have been written off. And much of that money was used to purchase discretionary toys, whether it was a new speedboat or hummer or, ironically, a second home or rental property.

Most of it was lost because it just wasn’t affordable.

And there was no need, because the majority of loans at the time were taken out with stated income loans or without documentary loans.

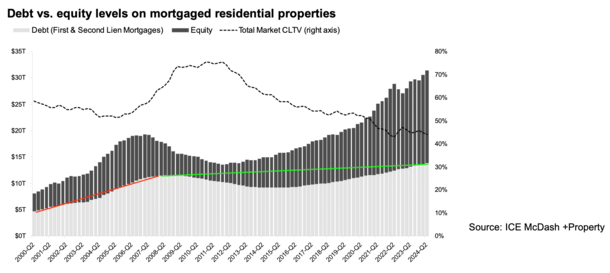

Outstanding mortgage debt is low compared to the early 2000s

Today, things are very different in the real estate market. Your typical homeowner has a 30-year fixed mortgage. Maybe they even have a fixed sentence of 15 years.

And chances are they have a mortgage interest rate between two and four percent. Maybe even lower. Yes, some owners have rates that start with a “1”.

Many of them also purchased their properties before the sharp rise in prices that preceded the pandemic.

The national LTV is therefore ridiculously low, less than 30%. In other words, for every million dollars of home value, a borrower only owes $300,000!

Just look at the graph of ICE this shows the huge gap between debt and equity.

Consider that your average homeowner has a ton of home equity that is mostly untapped, with the ability to take out a second mortgage and still maintain a significant cushion.

Long story short, many existing homeowners have taken on very little mortgage debt relative to the value of their property.

Despite this, we continue to suffer from an affordability crisis. Those who have not yet purchased often cannot afford it.

Home prices and mortgage rates are too high to qualify new home buyers.

The problem is that there’s no real reason for house prices to fall because existing homeowners are in such a good position. And there are too few properties available for sale.

Given high prices and low affordability, some believe we are in another bubble. But it is difficult to achieve this without funding.

And as noted, the financing has been pretty impeccable. He was also very conservative.

In other words, it’s hard to get a widespread crash where millions of homeowners fall behind on their mortgages.

At the same time, existing homeowners value their mortgages more than ever because they are so cheap.

Simply put, their current housing payment is the best option they have.

In many cases, it would be much more expensive to rent or purchase a replacement property. So they stay where they are.

Do we need a second wave of mortgage lending to bring down the housing market?

So how can we cause another housing market crash? Well, I’ve been thinking about this a lot lately.

Even though housing is no longer the “problem” this time around, as it was in the early 2000s, consumers are being put to the test.

There will come a time when many will need to borrow against their homes to pay for daily expenses.

This could involve taking out a second mortgage, such as a HELOC or home equity loan.

Assuming this happens en masse, you could see a situation where mortgage debt explodes.

At the same time, house prices could stagnate or even fall in some markets due to continued unaffordability and deteriorating economic conditions.

If that happens, we could end up in a situation where homeowners are overburdened again, with less equity serving as a cushion if they fall behind on their payments.

You could then have a real estate market filled with properties that are much closer to peaking, similar to what we saw in the early 2000s.

Of course, the big difference would still be the quality of the underlying home loans.

And first mortgages, which if left intact would remain very cheap fixed rate mortgages.

Even then, a major housing crash seems unlikely.

Of course, I could see more recent home buyers who didn’t get an ultra-low mortgage rate or a low purchase price, walk away from their properties.

But this time, most of the market is not made up of homeowners. Sales volume has been low since mortgage rates and prices have been high.

The fact is that we might still be in the early stages of the real estate cycle, strange as that may sound.

That is, if you want to base it on new mortgage debt (borrowing) this cycle.

Because if you look at the chart above, it’s clear that today’s homeowners simply haven’t borrowed much.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to start writing about mortgages 18 years ago to help potential (and existing) buyers better navigate the home loan process. Follow me on Twitter for hot takes.